Clients expect the current level of uncertainty to increase demand for external support — but…

Regular readers of this update will know that we’ve become more cautious of late, predicting that demand for consulting and other professional services, which has grown exceptionally strongly over the last 18 months, may soften somewhat in the second half of the year.

Our most recent research*, carried out in early August, suggests a more complex picture, with uncertainty driving growth rather than undermining it—for the moment.

Businesses are being hit by multiple shocks. The biggest negative impact is coming from high and/or rising energy costs: 26% of respondents say that these have either already had a strongly negative impact on their organisation or are likely to do so in the next six months. A further 37% say they’ve been impacted negatively by these rising fuel costs, albeit less severely. There are other factors at play too: high inflation, the cost of borrowing, uncertainty around the likelihood of a global recession, and supply–chain problems are each flagged by around one in five clients as having a severely negative impact.

The other side of this story is that three-quarters of client organisations still have more ambitious corporate goals post-pandemic than they had before COVID, and roughly the same proportion say they are confident about the future.

Just over a third of the clients we surveyed say that confidence is falling because their sales are down as customers economise. Twenty-three percent blame the fact they can’t get the raw materials and components they need. But external uncertainties aren’t the only factor here. Twenty-seven percent say that confidence is lower because they’re short of key staff; 17%, that they don’t think they can cope with their existing challenges, let alone these new ones; 14% say they’re still hampered by staff absences as a result of COVID. Conversely, organisations that haven’t suffered a loss of confidence are those that have the staff they need, continue to enjoy strong sales, and feel they can cope with the challenges they face.

“Just over a third of clients say that confidence is falling because their sales are down as customers economise.”

As a result of these challenges, 81% of clients say that their organisations will have to cut back on planned investments, with 28% anticipating making a significant reduction. This is true even in countries, such as the US, where the most recent economic indicators have been more positive. However, the changes required, combined with the shortage of in-house resources, mean that organisations will need more, not less support. Over two-thirds of clients say they’ll need more support from consulting firms, directly as a result of upheaval they’re facing. Moreover, the proportion of clients saying that, for the moment, they’ll need more consulting help in general has jumped from 52% three months ago to 66% now.

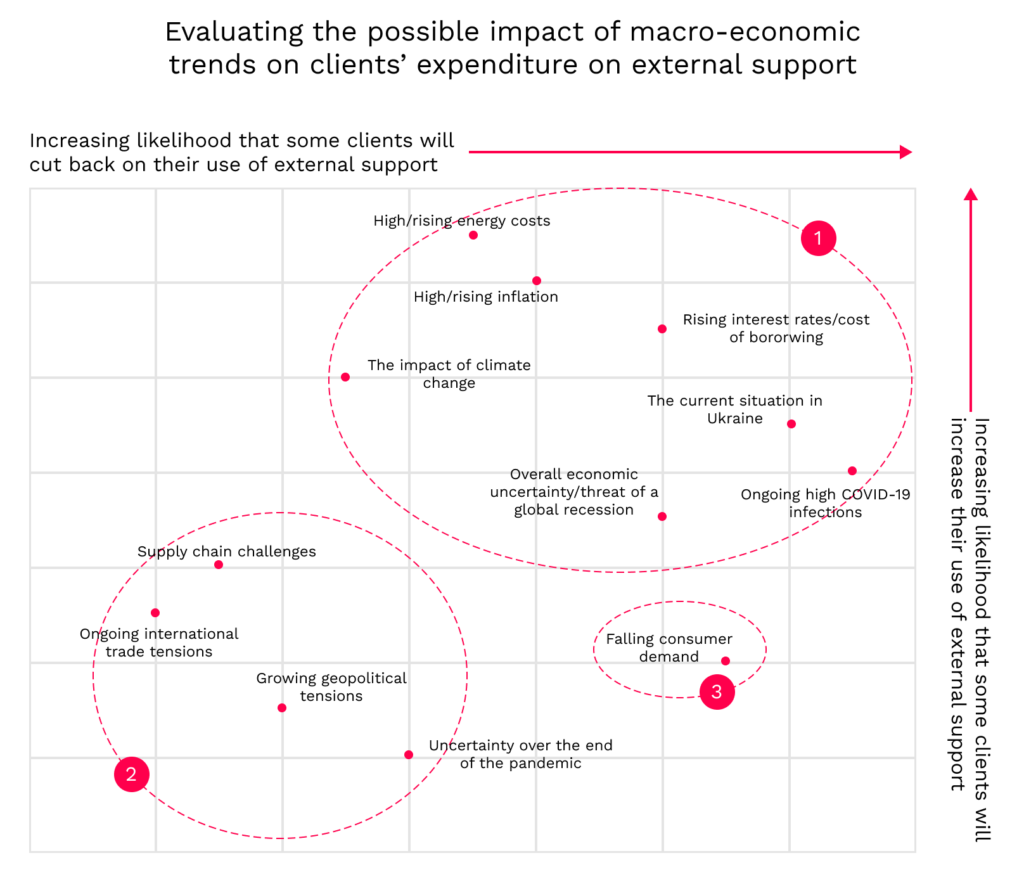

However, clients’ ability to make good on these predictions depends on the situation not getting worse. To gauge what might happen, we’ve analysed how clients might react to specific issues and have identified three distinct scenarios.

Consumers will have the final say

In our first scenario (see chart below — ❶), client behaviour will be mixed. Some organisations will reduce their expenditure on consulting services while others increase it, the one cancelling out the other. This applies to an environment where energy and other costs have spiralled steeply upwards, where the cost of borrowing has become significantly more expensive, where a deep global recession appears imminent, where climate change is having a significant impact on business operations, and/or where the COVID-infection rates rise again.

Clients appear to have already decided how to respond to the key problems in scenario ❷, which is set against a backdrop of supply-chain issues, international trade and political tensions, and uncertainty about the end of the pandemic. They’ve had time to adjust to these challenges—they are ‘known knowns’, in effect, meaning they’re less likely to have an impact on whether or not organisations turn to consulting support.

The most troubling scenario is ❸, as it appears that falling consumer demand—presumably translating into lower sales—is relatively likely to result in client organisations cutting back their expenditure on existing consulting services, and is relatively unlikely to drive demand for new, different ones.

In scenario ❶, uncertainty will probably increase the rate of growth in demand for consulting services, while in scenario two the chances are that it will have no impact either way. Scenario three could, however, bring down the rate of growth—so this is the one to watch.

This latest round of research suggests that clients are reasonably bullish that the savings accumulated by many households during the pandemic will cushion them from the immediate consequences of rising costs. Clients may be banking, too, on the current, high levels of inflation being short-lived. If these assumptions turn out to be wrong, consulting and other professional services firms will need to adapt as well.