Professional services firms need to start adapting to a multi-shock world

In our last update we discussed the probability that the rate of growth in the professional services sector, which has been exceptionally high since Q3 of 2020, will start to slow in the second half of this year, edged down by clients’ sense of macro-economic uncertainty that’s likely to impact some services more than others. The market is no longer, we concluded, a rising tide of growth that will lift all boats.

In the last two weeks we’ve sent out our quarterly survey to consulting firms, collecting responses from the very large to the fairly small, which backs up this prediction.

Although 86% of consulting firms say they’re confident about the consulting market in the second half of 2022, 24% firms are less confident now than they were at the end of Q1. The proportion of firms saying that their pipeline is stronger than it was three months ago has dropped from 74% to 55%., But this is only slightly worse than they were in Q4 2021, so it may be that the first quarter of this year was a misleading outlier. Asked why they think their pipeline is weaker than it was, the vast majority of firms pointed to a general sense that the global economy is heading for a recession; some also mentioned rising inflationary pressure and slowing momentum around revenue growth on the client side.

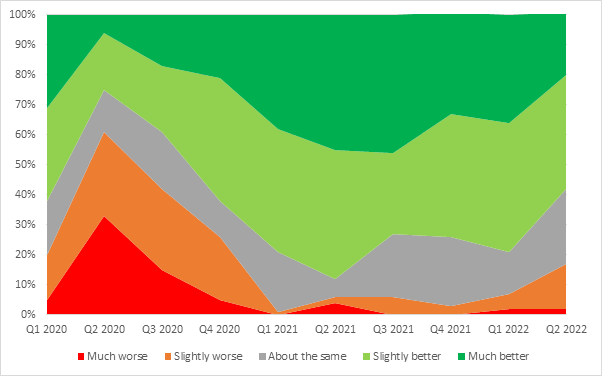

The chart below is the most up-to-date snapshot we have of the market at the moment. And what it suggests is that the peak of post-pandemic growth has passed. At its height, in Q2 last year, 88% of consulting firms said that their performance in that quarter had been higher than the previous one. The equivalent number today is 59%. Over the same time frame, the proportion of firms saying they’d performed worse compared to the previous quarter has almost tripled from 6% to 17%.

Clearly, this isn’t good news, but it’s not—yet—particularly bad news either, for three reasons. First, only 2% of firms describe themselves as being much worse off, and that number hasn’t been growing significantly. True, 15% say their performance has deteriorated slightly, but that’s not unusual in an industry in which stable revenues are rare and many firms habitually run on short orderbooks. Second, overall performance is now broadly in-line with what it was in Q1 2020, before the pandemic hit, and when the proportion of firms saying their performance had improved as 62%, so what we might be seeing here is a reversion to the historic mean. Finally, and most importantly, this chart shows quarter-on-quarter changes, not absolute values, so the lower percentage of firms saying they’re doing better are doing better against multiple quarters in which demand has grown exceptionally fast.

This supports our argument that, based on the available data, the rate of growth in the consulting industry is likely to slow in the second half of 2022—and where the consulting market leads, many other professional services markets follow. The psychological impact of this is likely to be greater than the economic: For professional service firms that have become accustomed over the last 18 months to almost continually rising growth rates this may feel like a shock, even if it’s simply returning the industry to its pre-COVID norm.

The deeper worry is that the rate of growth slows further—and here professional services firms need to learn from their clients. Clients are reacting to the daily accumulation of bad news as they did during the pandemic, only more quickly. After a short and inevitable period of paralysis, they’re deferring some projects but are also adapting to a multi-shock environment by turning to consultants for different services. Digital transformation still dominates, but demand for sustainability-related work is increasing alongside productivity improvement. As organisations feel their way to the right balance of hybrid working, the proportion of consulting firms being asked to help with cultural change has more than doubled. Regulation and risk are doing well, while M&A work has taken a hit—as has strategy to a lesser extent.

The message from this data, and from our other research, is clear. There is still plenty of growth in the market, but professional services firms need to start adapting now to the changes a multi-shock world will bring.

If you are a journalist or work for a news organisation and would like to reference our data, please get in touch with David Pippett at david@proservpr.com