The talent crisis in professional services: still here

For the last two updates, we’ve focused on the subtle shift taking place in the consulting and wider professional services market that’s likely to soften demand in the second half of the year.

Evidence from the supply side suggests that the proportion of firms whose quarter-on-quarter revenues increased in Q2 2022 is somewhat lower than in the first quarter of the year.

The percentage of clients who say they’ll spend more on consulting services in the next 12 months has fallen slightly compared to last year, but almost half of the clients we survey still expect their expenditure on consulting to increase over the next 12 months. Clients say that macro-economic uncertainty, especially high and rising inflation, is going to make it hard for them to deliver their more ambitious, post-pandemic plans. However, it’s not yet clear how that will impact spend on professional services in the future. Firms’ pipelines are growing less quickly, but 55% say that they are bigger than in the previous quarter.

But growth isn’t just determined by demand-side factors. Last summer, our research revealed that around a third of US clients had been unable to proceed with projects requiring the support of professional services firms because the latter didn’t have the capacity to do the work involved. When we asked firms themselves, one in five said they’d turned work down because they didn’t have the right skills/staff. At that point we argued that while growth might have been exceptionally high, it could have been even higher.

Are demand and supply more in sync than they were 12 months ago? If we look at demand data from professional services firms, 10% say that their pipeline at the end of Q2 is smaller than it was at the end of Q1—twice the proportion that were in this position three months earlier. At the same time, the percentage who say their pipeline grew in Q2, while still a healthy 55%, is down from 74% in the previous quarter. This throws weight behind our previous conclusions that the market is still growing well, but not quite as strongly as it was.

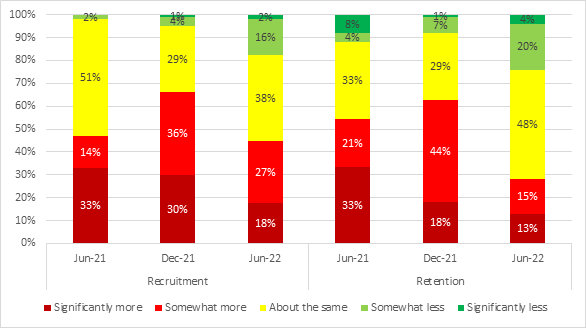

On the supply side of the equation, the situation is improving. At the end of June, 28% of firms said that their retention issues had further deteriorated in H1 2022, but this was down from the 62% who said that they’d deteriorated in the second half of 2021. Similarly, 45% of firms said the recruitment situation was worse in H1 2022 compared to H2 2021—still bad, but not as desperate as the 66% who said that H2 2021 was worse than the first half of that year. The situation is still deteriorating, but it’s not deteriorating as fast as it was.

Extent to which recruitment/retention have been greater problems for firms than in the previous six months

But the numbers don’t quite balance. Demand is higher (but not as high as it might have been) and supply, in the form of firms’ capacity to deliver work, is lower (but not as low as it might have been). Yet, when we ask firms whether they’re still turning work away, the proportion saying they’re doing so is down from one in five to one in 20.

Professional services firms are, in effect, doing more with less—and there are only two ways they can do this. First, they can be automating more of the work or at least using software tools that allow them to do large projects more efficiently and effectively.

While professional services firms, especially consulting firms, have been investing in such tools—both during the pandemic as they adapted to remote working, but also in its aftermath as they started to appreciate just how severe the talent crisis might be—it’s unlikely this strategy alone will have bridged the current gap between demand and supply. Not all types of consulting and other professional work lend themselves to automation, and the investment and consequent training take time.

The second part of the explanation is probably more important: The people delivering professional services are working harder and longer. They’re probably being paid more too—research we did earlier in the year suggested that two-thirds of firms had put up their salaries significantly in response to the problems they were facing around recruitment and retention. But, in an industry that already has a reputation for long hours, it’s unsustainable: More people will leave.

The talent crisis isn’t over yet.