Don’t underestimate the importance of staff augmentation

Using external support to do business-as-usual work has always been a key reason why organisations spend money with professional services firms—and it’s even more important today. But will it stay that way?

The professional services sector has grown on the back of client organisations’ need for capability and capacity. Capability in terms of specialist expertise that’s hard to find and therefore not typically available on the client side. Capacity in the form of competent generalists who can put their hand to almost any managerial task, and who can be brought in and sent away at short notice. Both create much-needed flexibility in a client’s organisational model, enabling the latter to access scarce skills and to cope with peak workloads as and when required.

Professional services firms see the picture somewhat differently, preferring to emphasise their specialist capabilities and to minimise the amount of “staff augmentation” work they do. The reason is straightforward: Margin. In our research across multiple markets this year, 52% of clients said that expertise was one of the main reasons why they’d be prepared to pay premium prices for a given piece of work. By contrast, staff augmentation is conventionally undertaken by generalists, often relatively junior people who’ve been taught how to manage projects but little else. Firms rarely turn capacity-driven work away because, by virtue of its flexibility, it can absorb people who haven’t been assigned to chargeable work. But carrying out a high proportion of “body shopping” damages a firm’s brand—clients see it as little better than a staffing agency—and reduces the rates it can charge across all its services.

It’s perhaps ironic then that one of the reasons for the exceptional growth enjoyed by consulting and other professional services over the last 18 months is that post-pandemic client organisations are short-staffed. Seventy-eight percent of clients on the same survey said that their workload has increased, while 72% said that the speed with which they must work has accelerated. At the same time, 67% said that many colleagues are stressed and exhausted by the aftermath of COVID; 53% that many of their colleagues had resigned in the last year; and 65% that they were finding it harder than ever to recruit. Overall, 60% described their organisations as being very short-staffed. Not surprisingly, more than twice as many clients cite capacity as the number one reason for using outside help than those who cite capability (68% to 27%, with 6% citing other reasons).

Clients’ shortage of staff continues to be a major reason why demand for consulting and other professional services has continued to be strong against a backdrop of economic uncertainty and despite the fact that three-quarters of clients say their ability to invest in the next 2-3 years is under threat.

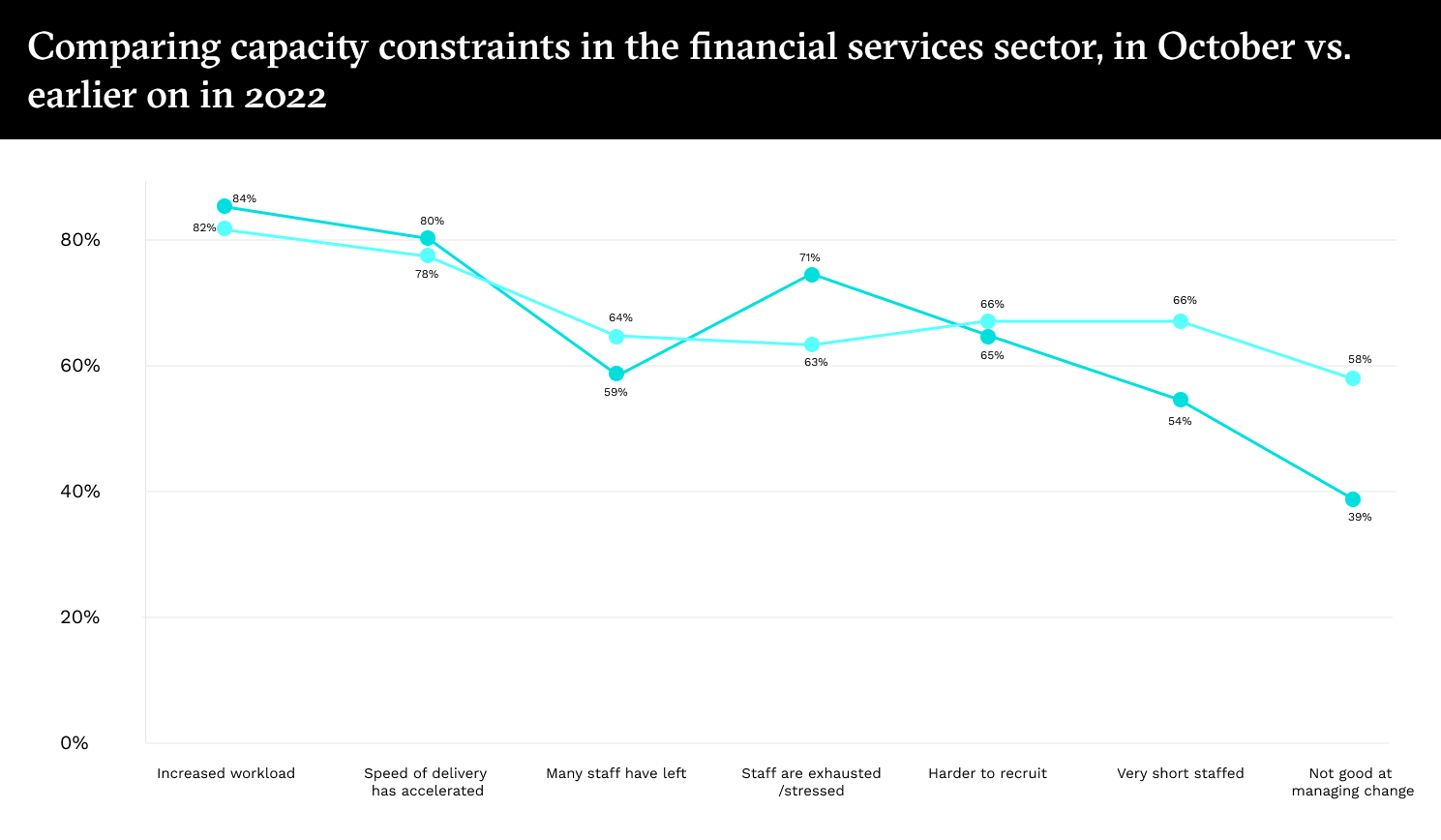

A critical question, therefore, is whether this will continue. Will client organisations, which are already short-staffed, find themselves having to make layoffs that exacerbate the situation? Or will the threat of rising unemployment at a time of high inflation draw people back into the workforce? Yet-to-be published data on the financial services sector, gathered by us in the last couple of weeks may give us a very early indication of what may happen.

The picture it paints is one in which workloads and the pace of activity remain problematically high, with staff even more exhausted and stressed. Recruitment remains difficult, however the number of people leaving may be coming down. As a result, the proportion of people who say that their organisation is short-staffed has fallen from 66% only a few months ago to 54% now. That has consequences for how effectively organisations are managing change, where the proportion of people saying that they’re not managing change well has fallen from 58% to 39%.

What this may point to—and we need to stress that this is one set of data about one sector—is that demand for staff augmentation may start to fall, potentially making the consulting and wider professional services industry somewhat less resilient. The change is likely to be gradual and it may be reversed, as clients recognise that they still need external support for capability reasons, as they did in the middle of 2020. But it does introduce a note of caution into what is still currently a high-growth market.

What this may point to—and we need to stress that this is one set of data about one sector—is that demand for staff augmentation may start to fall, potentially making the consulting and wider professional services industry somewhat less resilient. The change is likely to be gradual and it may be reversed, as clients recognise that they still need external support for capability reasons, as they did in the middle of 2020. But it does introduce a note of caution into what is still currently a high-growth market.